Like many other people, we got a cancellation letter from our health insurance carrier. It contains the same news people all over the country are getting.

Anthem Blue Cross and Blue Shield is discontinuing your individual health benefit plan because it doesn’t meet all the requirements of the new health care reform laws (also called the Affordable Care Act).

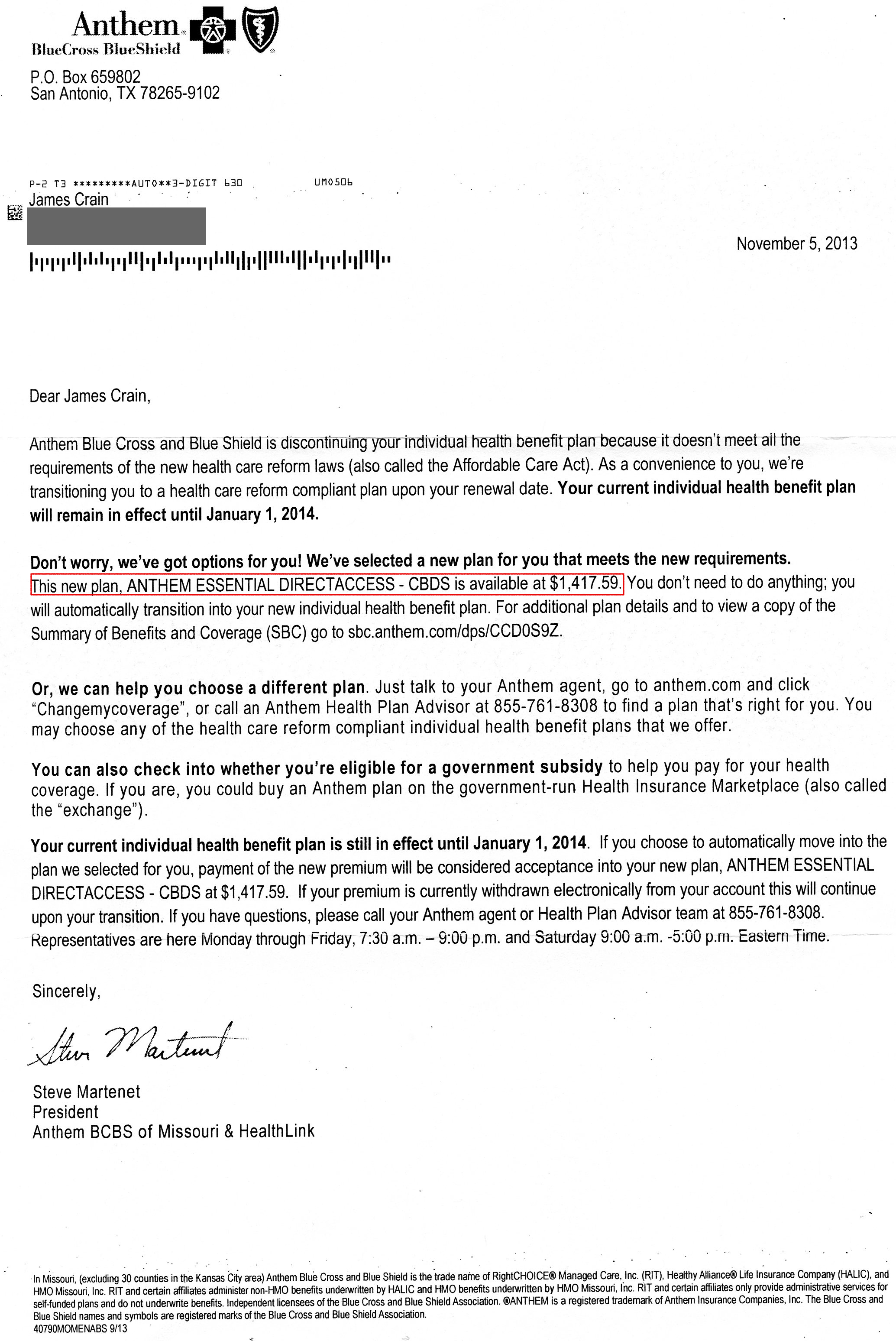

(Click for a larger, readable view.)

Are we upset? You bet!

1. Did the President and his administration lie about "if you like your plan, you can keep it"? That’s what NBC News reports.

And the Obama administration is still claiming that at this writing. I like the part on that page about how they’ll "debunk the myth that reform will force you out of your current insurance plan or force you to change doctors" since those are exactly the problems my family faces now.

2. The "Affordable Care Act" name is blackly humorous because this new plan we’re offered would cost more than twice what we currently pay for a plan with the same deductible. That $1,417.59 number in the letter would be our monthly cost.

A health care plan for three of us, for only $17,000 per year? What a deal!

3. I expected that a Federal bureaucracy would put itself in the business of deciding for the entire country what constitutes an "acceptable" health care plan and would then force everyone to buy one like that. And so it happened. At our ages, my wife and I don’t need maternity and newborn care but those "must be included on all non-grandfathered plans at no out-of-pocket limit."

I get the principle of pooling risk behind insurance. And it’s obvious that forcing everyone to pay for maternity and newborn care is a way to lower the cost for those who actually need it. Plus, the Democrats get the political advantage of saying that they’ve addressed "Womens Health" issues (by plundering everyone else).

The point is that the decision used to be taken freely; now it’s a compulsory action decided by a bureaucracy.

I’m sure that many would say, "But now young people will be sharing the risk of your age-related care too." That’s likely true as well. But I don’t think the young folks should be compelled to do that. If I had my way, I wouldn’t be forcing my sons (and their peers) to pay my bills.

The fix that the US health care system needed was more price transparency so patients could make better-informed decisions. Just try asking your doctor or dentist what the costs will be beforehand. If your experience is like mine, you’ll get blank looks and people who ask "Why do you care? You’re not paying for it."

It’s a fact that my dentist charges me only half of what he charges an insurance company for a check-up and cleaning. Those days are gone now.

I don’t expect that transparent prices will be a panacea. Transparency won’t solve cases of life-and-death urgency nor will it make everyone medically literate when shopping for a doctor. But I don’t think there’s any perfect solution for all cases. Remember: hard cases make bad law.

Price transparency is what’s needed to allow the market to work despite those counter factors. Why do prices for procedures not typically covered by insurance plans ("elective procedures") keep falling? Markets at work.

But PPACA goes in the opposite direction. Not only does it fail to fix the pricing problem, it entrenches and effectively subsidizes the current system of hiding price information. Welcome to the one-size-fits-all-means-it-fits-nobody world.

4. But what has me most angry is not President Obama nor the Democratic Party congressmen who saddled us with this disaster. They only did what they’ve been saying for years that they’d do. Instead, I’m upset with all of those people who voted to put Obama and his party in power.

So instead of sarcastically saying, "Thanks, Obama!" what I’ll say sarcastically is, "Thanks a lot, Fellow Voters!" Thank you so very much for forcing us all to join a health care buyers’ club whether we wanted it or not.

Do not blame Caesar, blame the people of Rome who have so enthusiastically acclaimed and adored him and rejoiced in their loss of freedom and danced in his path and gave him triumphal processions and laughed delightedly at his licentiousness and thought it very superior of him to acquire vast amounts of gold illicitly. Blame the people who hail him when he speaks in the Forum of the ‘new, wonderful good society’ which shall now be Rome’s, interpreted to mean ‘more money, more ease, more security, more living fatly at the expense of the industrious.

I don’t know who said this but it describes the state of affairs all too well. It’s often attributed to Cicero (but there’s some dispute about that).